Unknown Facts About Bankruptcy Lawyer Tulsa

Table of ContentsFacts About Bankruptcy Attorney Tulsa UncoveredThe Greatest Guide To Bankruptcy Attorney TulsaHow Tulsa Debt Relief Attorney can Save You Time, Stress, and Money.The Best Guide To Tulsa Bankruptcy Filing AssistanceSee This Report about Affordable Bankruptcy Lawyer Tulsa

The stats for the other primary kind, Phase 13, are also worse for pro se filers. (We break down the distinctions in between the 2 types in depth listed below.) Suffice it to claim, speak to a legal representative or 2 near you who's experienced with personal bankruptcy legislation. Here are a couple of sources to locate them: It's easy to understand that you could be hesitant to spend for an attorney when you're already under substantial economic stress.Several attorneys also supply cost-free examinations or email Q&A s. Make the most of that. (The non-profit application Upsolve can aid you discover complimentary examinations, resources and legal assistance absolutely free.) Ask them if bankruptcy is certainly the ideal option for your circumstance and whether they think you'll qualify. Prior to you pay to submit personal bankruptcy kinds and acne your credit record for approximately 10 years, check to see if you have any type of viable options like financial obligation settlement or charitable credit history counseling.

Ads by Cash. We may be made up if you click this ad. Ad Since you have actually decided personal bankruptcy is undoubtedly the ideal course of action and you hopefully removed it with a lawyer you'll require to begin on the paperwork. Prior to you dive into all the official bankruptcy types, you should get your own documents in order.

Tulsa Bankruptcy Legal Services Things To Know Before You Get This

Later on down the line, you'll actually require to show that by revealing all sorts of info about your financial affairs. Below's a basic listing of what you'll require when driving ahead: Identifying records like your vehicle copyright and Social Security card Tax returns (up to the previous four years) Proof of income (pay stubs, W-2s, freelance earnings, income from possessions along with any kind of income from federal government benefits) Financial institution statements and/or retired life account declarations Proof of worth of your properties, such you could look here as lorry and realty appraisal.

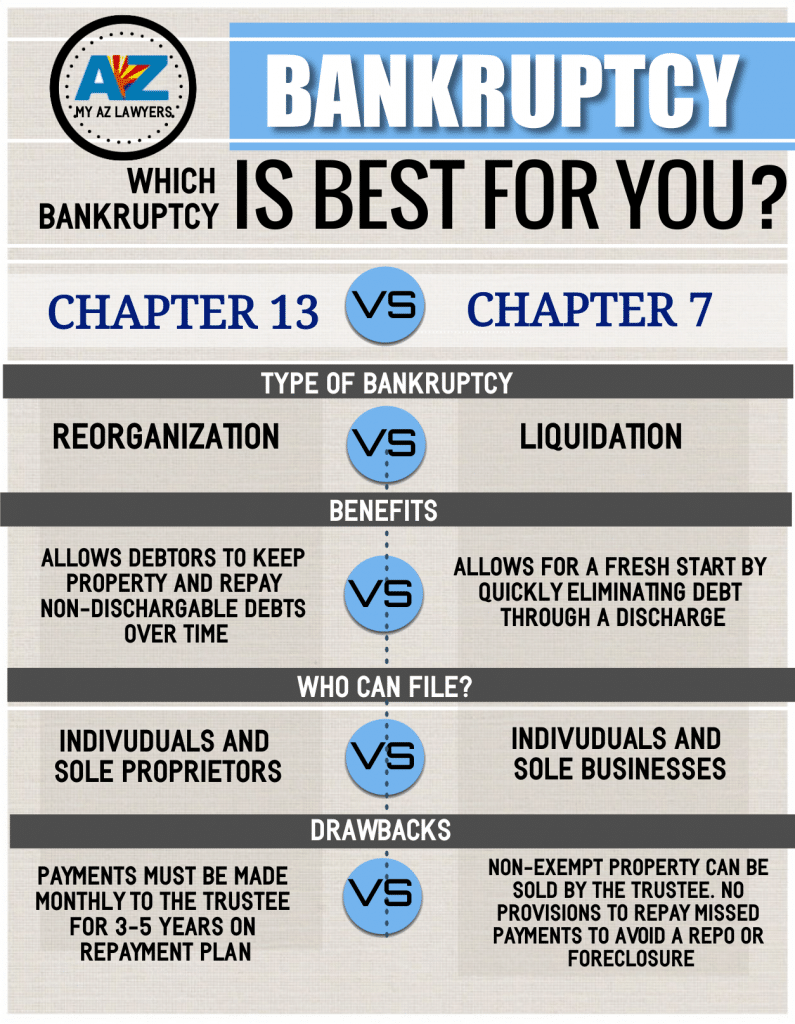

You'll want to understand what kind of financial obligation you're attempting to settle.

You'll want to understand what kind of financial obligation you're attempting to settle.If your revenue is also high, you have one more option: Chapter 13. This choice takes longer to settle your financial obligations since it requires a long-term payment strategy generally three to 5 years before a few of your continuing to be financial debts are wiped away. The filing process is likewise a great deal a lot more complex than Chapter 7.

Bankruptcy Attorney Near Me Tulsa Fundamentals Explained

A Phase 7 personal bankruptcy remains on your credit rating report for 10 years, whereas a Chapter 13 insolvency drops off after seven. Both have enduring effect on your credit history, and any kind of brand-new financial obligation you take out will likely come with greater rates of interest. Prior to you send your personal bankruptcy types, you must first finish a compulsory training course from a credit report therapy company that has been accepted by the Division of Justice (with the significant exception of filers in Alabama or North Tulsa bankruptcy attorney Carolina).

The training course can be completed online, personally or over the phone. Training courses usually cost in between $15 and $50. You should finish the program within 180 days of declare insolvency (bankruptcy lawyer Tulsa). Use the Division of Justice's web site to find a program. If you stay in Alabama or North Carolina, you have to choose and complete a program from a list of separately accepted providers in your state.

The 3-Minute Rule for Best Bankruptcy Attorney Tulsa

Inspect that you're filing with the appropriate one based on where you live. If your irreversible house has actually relocated within 180 days of filling up, you need to file in the district where you lived the higher portion of that 180-day duration.

Usually, your personal bankruptcy attorney will function with the trustee, yet you might need to send the person documents such as pay stubs, tax obligation returns, and bank account and debt card declarations directly. A common misconception with personal bankruptcy is that as soon as you file, you can quit paying your debts. While insolvency can aid you wipe out many of your unprotected debts, such as past due medical bills or individual fundings, you'll desire to maintain paying your monthly repayments for protected financial obligations if you want to keep the building.

Indicators on Chapter 7 Vs Chapter 13 Bankruptcy You Should Know

If you go to threat of foreclosure and have tired all other financial-relief choices, then declaring Phase 13 might delay the repossession and help save your home. Eventually, you will certainly still require the income to proceed making future home loan repayments, along with paying back any late repayments over the course of your settlement plan.

The audit can delay any type of financial debt alleviation by several weeks. That you made it this far in the procedure is a respectable indicator at the very least some of your debts are eligible for discharge.